Last updated: June 7, 2026

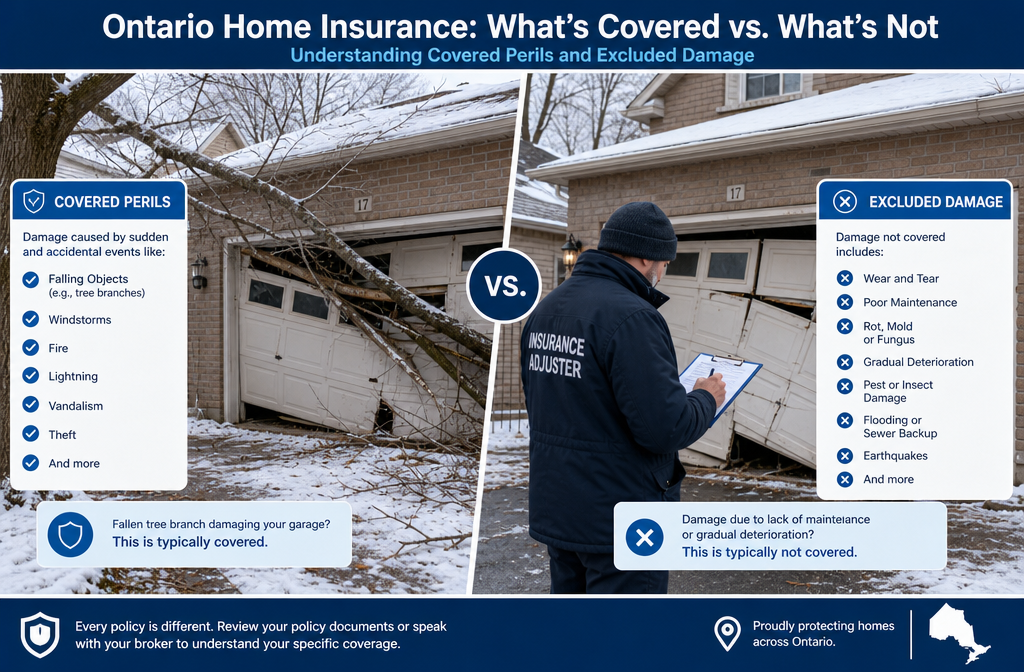

Quick Answer: Home insurance in Ontario typically covers garage door damage caused by sudden, unexpected events such as storms, vehicle impact, fire, or vandalism. Damage from normal wear and tear, mechanical failure, or poor maintenance is almost always excluded. Whether a specific claim is approved depends on the cause of damage, your policy type, and whether your deductible makes a claim financially worthwhile.

Key Takeaways

- Most standard Ontario home insurance policies cover garage doors under the “other structures” or dwelling section, but only for named or listed perils.

- Sudden events like windstorms, hail, falling trees, vehicle collisions, and break-in damage are commonly covered causes.

- Wear and tear, rust, mechanical breakdown, and gradual deterioration are almost always excluded.

- Detached garages may have separate or reduced coverage limits, often capped at 10% of the main dwelling coverage.

- Filing a claim can affect your premium at renewal, so compare the repair cost against your deductible before proceeding.

- Documentation is critical: photos, repair estimates, and a written incident description all strengthen a claim.

- The average garage door insurance claim in Ontario takes two to six weeks to resolve, though complex cases can take longer.

- You can purchase endorsements or floaters for broader garage door protection, which is worth considering for high-value custom doors.

What Types of Garage Door Damage Are Typically Covered by Home Insurance in Ontario

Standard Ontario home insurance covers garage door damage that results from a sudden, accidental, and external cause. The most commonly covered events include windstorms, hail, falling trees or branches, fire, lightning, vehicle impact (including your own vehicle backing into the door), vandalism, and theft-related damage such as a forced entry that breaks the door.

Covered perils most commonly seen in Ontario claims:

- Wind and storm damage (including ice storms and severe hail)

- Falling objects such as tree limbs or ice buildup from the roofline

- Vehicle collision with the door or frame

- Fire or smoke damage

- Vandalism or malicious damage

- Break-in damage where the door was forced open

Coverage depends on whether you have a “named perils” or “all-risk” (comprehensive) policy. An all-risk policy covers any cause of damage that is not explicitly excluded, which provides broader protection. A named perils policy only covers causes that are specifically listed. Most Ontario homeowners carry all-risk policies, but it is worth confirming with your broker.

Choose all-risk coverage if you want the broadest protection and your insurer offers it at a reasonable premium increase. Named perils policies are cheaper but leave gaps that matter when something unusual damages your door.

How Much Does a Standard Garage Door Repair Cost Without Insurance

Without insurance, garage door repair costs in Ontario vary widely based on the type and extent of damage. Minor repairs such as cable replacement or panel dents typically run between $150 and $400. Spring replacement, one of the most common repairs, generally costs between $200 and $450 depending on the spring type and whether both springs need replacing. Full door replacement ranges from roughly $900 to $3,500 or more for a standard residential door, with custom or insulated models pushing costs higher.

For a detailed breakdown of spring-related costs, see this guide on garage door spring replacement costs in Oakville in 2026.

Typical repair cost ranges (Ontario, 2026 estimates):

| Repair Type | Estimated Cost (CAD) |

|---|---|

| Single panel replacement | $250 – $600 |

| Spring replacement (one spring) | $200 – $350 |

| Cable replacement | $150 – $300 |

| Opener repair or replacement | $150 – $500 |

| Full door replacement (standard) | $900 – $3,500+ |

| Storm or collision damage repair | $400 – $2,500+ |

These figures matter for insurance decisions because most Ontario home insurance policies carry deductibles between $500 and $2,500. If the repair cost is close to or below your deductible, paying out of pocket and avoiding a claim record is usually the smarter financial move.

Do I Need Special Coverage for Detached Garage Door Damage

Detached garages are covered differently from attached garages in most Ontario home insurance policies. An attached garage is generally treated as part of the dwelling and covered under the main structure limit. A detached garage is classified as an “other structure” and is typically covered at a sub-limit, commonly 10% of the dwelling coverage amount.

For example, if your home is insured for $600,000, your detached garage (including its door) may only be covered up to $60,000. For most standard garage doors, that limit is more than sufficient. However, if you have a custom carriage-house door or a large multi-car garage with high-end doors, that sub-limit could fall short of full replacement cost.

When to consider an endorsement for your detached garage:

- The detached garage contains expensive vehicles or equipment

- You have installed a custom or premium garage door worth more than $3,000

- Your current “other structures” sub-limit is below the replacement value of the structure

- You use the detached garage as a workshop or home-based business space (which may require a separate commercial rider)

Ask your broker to confirm whether your detached garage door is covered under the dwelling section or the other structures section, and what the applicable limit is. For homeowners with premium installations, the custom garage door options available in Oakville illustrate just how quickly door values can exceed standard sub-limits.

What Are Common Reasons Insurance Might Reject a Garage Door Claim

Insurance companies deny garage door claims most often because the damage falls under an excluded cause, particularly wear and tear or lack of maintenance. Understanding why claims get rejected helps homeowners avoid filing claims that will be denied and potentially flagged on their insurance record.

Most common reasons for claim denial:

- Wear and tear: Gradual deterioration of panels, hinges, or springs over time is not a covered peril.

- Mechanical or electrical failure: A broken torsion spring that snaps from age, or an opener that burns out, is typically excluded.

- Pre-existing damage: If the insurer’s adjuster finds evidence the door was already damaged before the reported incident, the claim may be denied or reduced.

- Lack of maintenance: Rust, rot, or corrosion that develops because the door was not properly maintained is excluded.

- Intentional damage: Damage caused deliberately by the homeowner or a family member is not covered.

- Business use exclusions: If the garage is used commercially without a business rider, coverage may be voided.

- Policy lapse or non-payment: A lapsed policy at the time of damage means no coverage applies.

Edge case to watch: If a storm weakens your door and it then fails a few days later, insurers may argue the failure was mechanical rather than storm-related. Document the sequence of events carefully and report damage promptly to avoid this dispute.

Are Garage Door Repairs from Storm Damage Always Covered

Storm damage to garage doors is covered under most Ontario home insurance policies, but not automatically and not in every situation. The storm must meet the threshold of a “sudden and accidental” event. Windstorms, hail, ice storms, and falling trees or branches caused by a storm are standard covered perils.

However, several conditions can complicate a storm damage claim:

- Pre-existing weakness: If the door was already damaged, rusted, or poorly maintained, the insurer may argue the storm only accelerated an existing problem and reduce or deny the payout.

- Flood damage: Water that enters through a damaged door during a storm may not be covered if the water source is classified as a flood (overland water), which requires a separate endorsement in Ontario.

- Gradual water intrusion: Repeated water infiltration around door seals is considered a maintenance issue, not storm damage.

- Named storm deductibles: Some policies have higher deductibles for specific named storm events, though this is more common in coastal regions than inland Ontario.

If your garage door sustained storm damage, getting a professional inspection and written repair estimate quickly is important. For urgent situations, emergency garage door repair services can provide same-day assessment and documentation to support your claim.

What Documentation Do I Need to File a Successful Garage Door Insurance Claim

Strong documentation is the single most controllable factor in a successful garage door insurance claim. Insurers need evidence of what happened, when it happened, and what it will cost to fix.

Documentation checklist for a garage door insurance claim:

- Photographs and video: Take clear photos of all damage from multiple angles immediately after the incident. Include wide shots showing the full door and close-ups of specific damage points.

- Date and time record: Note exactly when the damage occurred or when you first discovered it.

- Written incident description: Write a brief, factual account of what happened. Avoid speculation about cause.

- Weather records: For storm claims, save screenshots of Environment Canada weather data or news reports confirming the storm event in your area on that date.

- Police report: Required for vandalism or break-in claims. File this before contacting your insurer.

- Repair estimates: Obtain at least two written estimates from licensed contractors. Insurers expect itemized quotes.

- Proof of ownership and value: For high-value custom doors, keep receipts or installation invoices in a safe place.

- Your policy documents: Know your deductible, coverage limits, and any relevant exclusions before you call.

If your door needs immediate securing after a break-in or storm, contact a repair service right away and keep all receipts. Most policies cover emergency mitigation costs. You can find same-day emergency garage door repair in Oakville and surrounding areas if you need urgent help while gathering claim documentation.

Will My Insurance Rates Go Up If I Make a Garage Door Claim

Filing a garage door insurance claim can increase your premium at renewal, though the impact varies by insurer, your claims history, and the size of the claim. In Ontario, insurers are permitted to use claims history as a rating factor. A single small claim may have minimal effect, but multiple claims within a short period can trigger a noticeable rate increase or even a non-renewal notice.

Factors that influence whether a claim affects your rate:

- Claims frequency: One claim in five years is treated very differently from two or three claims in two years.

- Claim amount: A $400 repair claim that barely exceeds your deductible is rarely worth filing. A $3,000 storm damage claim usually is.

- Fault determination: At-fault claims (such as backing your car into the door) may be weighted more heavily than not-at-fault claims.

- Your insurer’s specific policy: Some insurers offer “claims forgiveness” for first-time claims, which protects your rate after one incident.

Practical rule: If the repair cost is less than twice your deductible, pay out of pocket. For example, if your deductible is $1,000 and the repair is $1,200, you would only receive $200 from the insurer while still recording a claim on your history. The math rarely works in your favor for small claims.

How Long Does a Typical Garage Door Insurance Claim Process Take

Most straightforward garage door insurance claims in Ontario are resolved within two to six weeks from the date of filing. Simple claims with clear documentation and an obvious covered cause (such as a tree falling on the door during a documented storm) tend to move faster. Complex claims involving disputed causes, large dollar amounts, or contractor disagreements can stretch to several months.

Typical claim timeline:

| Stage | Typical Timeframe |

|---|---|

| Initial claim filing | Same day as damage |

| Insurer acknowledgment | 1 to 3 business days |

| Adjuster assigned | 3 to 7 business days |

| Adjuster inspection | 5 to 14 business days |

| Coverage decision | 1 to 3 weeks after inspection |

| Payment issued | 1 to 2 weeks after approval |

To speed up the process:

- File the claim as soon as possible after the damage occurs

- Have all documentation ready before the adjuster visits

- Respond promptly to any requests for additional information

- Do not authorize permanent repairs until the adjuster has inspected the damage (temporary emergency repairs are fine and should be done to prevent further loss)

What Garage Door Damages Are Usually Considered Wear and Tear

Wear and tear refers to the gradual deterioration that happens to any mechanical or structural component over time through normal use. Insurance policies across Ontario universally exclude wear and tear because it is a predictable, preventable outcome of aging, not a sudden or accidental event.

Common garage door issues classified as wear and tear:

- Spring fatigue and eventual breakage from repeated cycling (torsion and extension springs have a finite cycle life)

- Cable fraying or snapping from age and tension stress

- Rust and corrosion on panels, tracks, or hardware

- Weatherstripping deterioration

- Panel warping from moisture exposure over years

- Opener motor burnout from age

- Roller wear and track misalignment from extended use

If your garage door spring breaks after years of normal use, that is a wear and tear exclusion. If a spring breaks because a vehicle struck the door and bent the track, the spring failure may be covered as part of the collision damage. The cause matters more than the component.

Regular maintenance, including lubrication and annual tune-ups, creates a documented record that you have been maintaining the door properly. This can be useful if an insurer tries to attribute storm damage to neglect. See what a garage door tune-up actually involves to understand what maintenance records you should be keeping.

Steps to Take Immediately After Your Garage Door Gets Damaged

The actions taken in the first hour after garage door damage directly affect both the safety of your home and the outcome of your insurance claim. Acting quickly and methodically protects both.

Immediate steps after garage door damage:

- Ensure safety first. If the door is structurally unstable, keep people and vehicles away from it. A partially collapsed door can fall without warning.

- Photograph everything before touching anything. Capture the full scene, close-up damage, and any contributing factors (fallen branch, vehicle position, storm debris).

- Secure the opening. If the door cannot close or lock, arrange temporary boarding or contact an emergency repair service to prevent unauthorized entry.

- Document the cause. Save weather alerts, note the time, and write down what you observed.

- Call your insurer to report the damage. Most Ontario insurers have 24-hour claims lines. Reporting promptly is often a policy requirement.

- Get a written repair estimate. Contact a licensed garage door contractor for an itemized quote. This estimate goes to the adjuster.

- Keep all receipts. Any emergency repair costs, boarding materials, or temporary security measures should be documented for reimbursement.

If you notice warning signs before a full failure, such as grinding noises, uneven movement, or visible cable damage, addressing them early is both safer and cheaper. Reviewing signs that indicate immediate garage door repair is needed can help you catch problems before they become insurance-level events.

How Do Insurance Adjusters Evaluate Garage Door Damage

An insurance adjuster’s job is to determine whether the damage is covered under the policy, estimate the cost to repair or replace, and identify any contributing factors that might affect the payout. Understanding their process helps homeowners present their claim effectively.

What adjusters look for during a garage door inspection:

- Cause of damage: Is it consistent with the reported cause? Storm damage leaves specific patterns (impact from above, wind direction evidence). Vehicle impact leaves different marks than vandalism.

- Pre-existing condition: Signs of rust, prior dents, or deferred maintenance that existed before the reported incident.

- Scope of damage: Is only the door affected, or is the frame, track, opener, or structure also damaged? All affected components should be included in the claim.

- Repair vs. replacement: Adjusters determine whether repair is feasible or whether full replacement is necessary. For older doors, they may apply depreciation.

- Contractor estimates: Adjusters compare your submitted estimates against their own cost databases. Large discrepancies may trigger a second opinion.

Actual cash value vs. replacement cost value: Some Ontario policies pay out actual cash value (ACV), which accounts for depreciation. Others pay replacement cost value (RCV), which covers the full cost of a new equivalent door. Check your policy wording carefully. A 10-year-old door may have significant depreciation applied under an ACV policy, leaving you to cover the gap.

Difference Between Homeowners Insurance and Garage Door-Specific Coverage

Standard homeowners insurance in Ontario covers garage doors as part of the broader property policy, subject to all the standard exclusions. Garage door-specific coverage, sometimes offered as a home warranty or mechanical breakdown endorsement, covers different types of damage.

| Feature | Homeowners Insurance | Home Warranty / Mechanical Breakdown |

|---|---|---|

| Storm damage | Covered (named or all-risk) | Not covered |

| Vehicle impact | Covered | Not covered |

| Vandalism | Covered | Not covered |

| Spring/cable failure from age | Not covered | Often covered |

| Opener motor failure | Not covered | Often covered |

| Wear and tear | Excluded | Core coverage |

| Annual cost | Part of home premium | $300 – $700/year separately |

The two products are complementary, not competing. Homeowners insurance handles sudden, external damage. A home warranty or mechanical breakdown endorsement handles the gradual failures that home insurance excludes. For homeowners with older doors or openers, combining both types of coverage closes most of the gaps.

Who Should Consider Extra Garage Door Protection in Ontario

Not every homeowner needs supplemental garage door coverage, but certain situations make it worth the added cost.

Consider extra protection if:

- Your garage door is more than 10 years old and components are approaching end-of-life

- You have a custom or high-value door where replacement cost exceeds standard policy sub-limits

- Your home insurance deductible is high enough that most repair scenarios fall below it

- You live in an area of Ontario with frequent ice storms, heavy snowfall, or high wind events

- Your garage door is used frequently (multiple vehicles, high daily cycle count) accelerating component wear

- You rely on the garage as the primary home entry point, making any failure a security and access issue

For homeowners in areas like Oakville, Burlington, or Mississauga where severe winter weather is common, the risk of storm-related damage is real. Reviewing your current policy limits and deductible against realistic local repair costs is a practical annual exercise.

Frequently Asked Questions

Does my Ontario home insurance cover it if I accidentally back my car into my garage door? Yes, in most cases. Vehicle impact, including damage caused by your own vehicle, is typically a covered peril under standard Ontario home insurance. The claim would fall under your home policy (not auto), and your home deductible would apply.

Is a broken garage door spring covered by insurance? Almost never, unless the spring broke as a direct result of a covered peril like a vehicle collision or storm impact. A spring that breaks from normal fatigue and age is a wear and tear exclusion. For spring repair costs and options, see this guide on garage door spring repair.

What if my garage door was damaged during a break-in? Yes, break-in damage is covered under the vandalism or malicious damage section of most Ontario home policies. File a police report first, then contact your insurer. Keep the damaged door intact until the adjuster inspects it.

Can I choose my own contractor for a garage door insurance repair? Generally, yes. Ontario homeowners are not required to use insurer-preferred contractors, though your insurer may have a preferred network. You have the right to obtain independent estimates. The insurer will pay the reasonable cost of repair based on market rates.

Does insurance cover garage door panel replacement without replacing the full door? It depends on the extent of damage and whether matching panels are available. If only one or two panels are damaged and replacements are available, the insurer will typically pay for panel replacement only. If the door model is discontinued or panels cannot be matched, full replacement may be warranted. Learn more about garage door panel replacement options.

What happens if my garage door opener is also damaged in a covered event? If the opener is damaged as part of a covered claim (for example, a vehicle impact that damages both the door and the opener), the opener repair or replacement should be included in the claim. Standalone opener failure from age is not covered. For opener repair information, see garage door opener repair services.

How do I know if my deductible makes a claim worthwhile? Subtract your deductible from the total repair cost. If the net payout is less than $500, paying out of pocket and preserving your claims record is usually the better financial decision. If the net payout is $1,000 or more, filing is likely worth it.

Are garage doors covered during a power outage if the opener fails? No. Power outages and their effects on openers are not covered perils. However, battery backup openers can prevent access issues during outages. Read more about battery backup garage door openers and Ontario power outages.

Does filing a garage door claim affect my home insurance renewal? It can. Ontario insurers use claims history as a rating factor. A single claim may have minimal impact, especially if you have a clean history, but multiple claims can increase premiums or prompt non-renewal. Always weigh the net payout against the long-term premium cost.

What if the damage happened gradually over time rather than in one event? Gradual damage is not covered. Home insurance requires that damage be sudden and accidental. If a door slowly deteriorated from moisture, rust, or repeated minor impacts over months, that is treated as a maintenance issue and excluded.

Conclusion

Garage door insurance claims in Ontario follow a clear logic: sudden, external, and accidental causes are covered; gradual deterioration and mechanical failure are not. The most important steps any Ontario homeowner can take are to know their policy type, understand their deductible, and document damage thoroughly the moment it occurs.

Actionable next steps:

- Pull out your current home insurance policy and confirm whether you have all-risk or named perils coverage, and what your “other structures” sub-limit is for a detached garage.

- Check your deductible and compare it against realistic local repair costs so you know in advance when a claim is financially worthwhile.

- If your garage door is more than 10 years old, get a professional inspection to document its current condition. This creates a maintenance record that supports future claims.

- For storm damage or vehicle impact, photograph everything immediately, file a police report if vandalism is involved, and contact your insurer before authorizing permanent repairs.

- If you have a high-value or custom door, ask your broker about increasing your other structures sub-limit or adding a mechanical breakdown endorsement.

When damage does occur, getting a professional assessment quickly helps both the repair process and the insurance claim. For urgent situations across the Greater Toronto Area and surrounding communities, same-day garage door repair services can provide the inspection reports and written estimates that insurers require.